Magic Heidi

All-in-One für Schweizer Freelancer

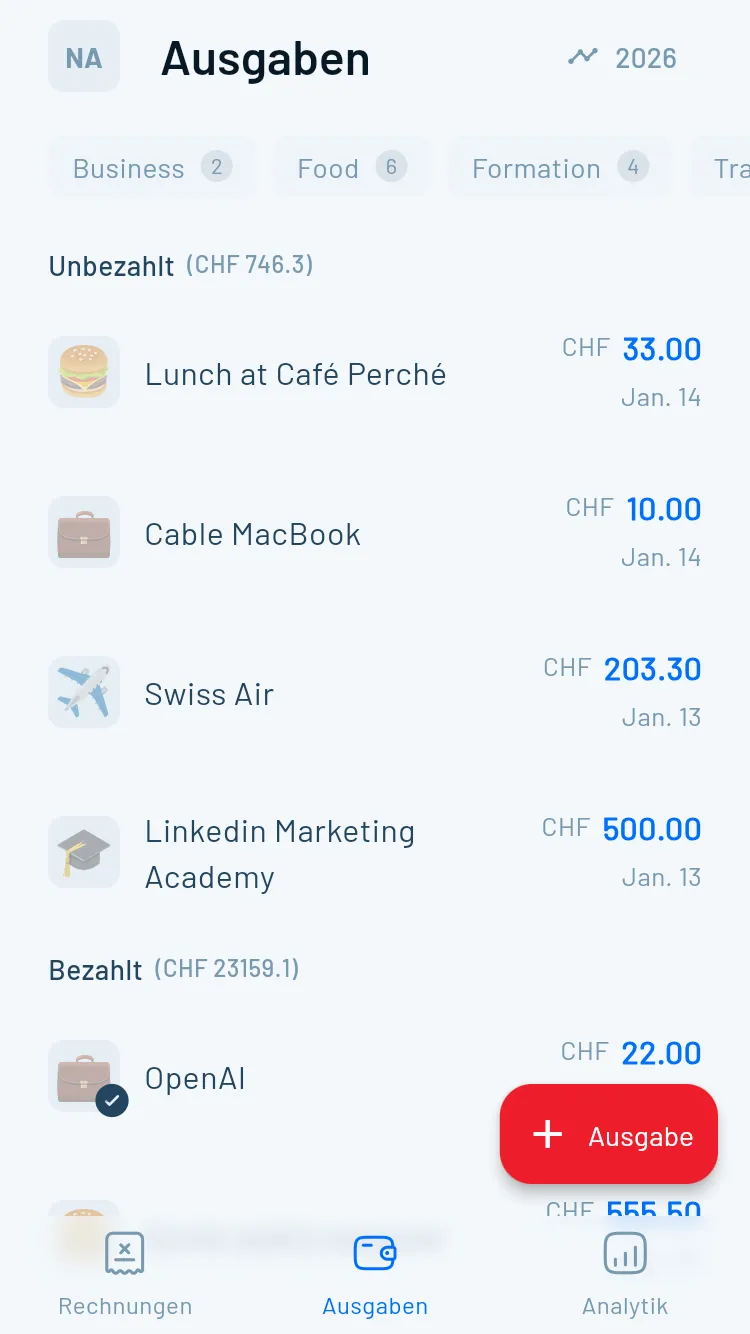

Ein Traum wird wahr für Schweizer Freelancer. Magic Heidi ist nicht nur eine Budget-App, sondern eine komplette Geschäftsverwaltung für Selbstständige. Die App wurde speziell für den Schweizer Markt entwickelt und deckt alles ab: von der Rechnungsstellung bis zur Ausgabenverfolgung.

- Schweizer Rechnungen in Sekunden: QR-Code-Zahlungsscheine nach Schweizer Standards, automatische MwSt.-Berechnung

- KI-gestützte Ausgabenverfolgung: Belege fotografieren, fertig. Die AI erkennt automatisch Datum, Betrag und Kategorie

- Integrierte Steuer- und Buchhaltungstools: Steuerschätzung, Rücklagenplanung, Export für Treuhänder

- Verfügbar: iOS, Android, Web, Mac, Windows | Sprachen: DE, FR, IT, EN, ES, PT | Preis: Kostenlose Testversion, dann Abo