Schritt 1

Finanzunterlagen zusammenstellen

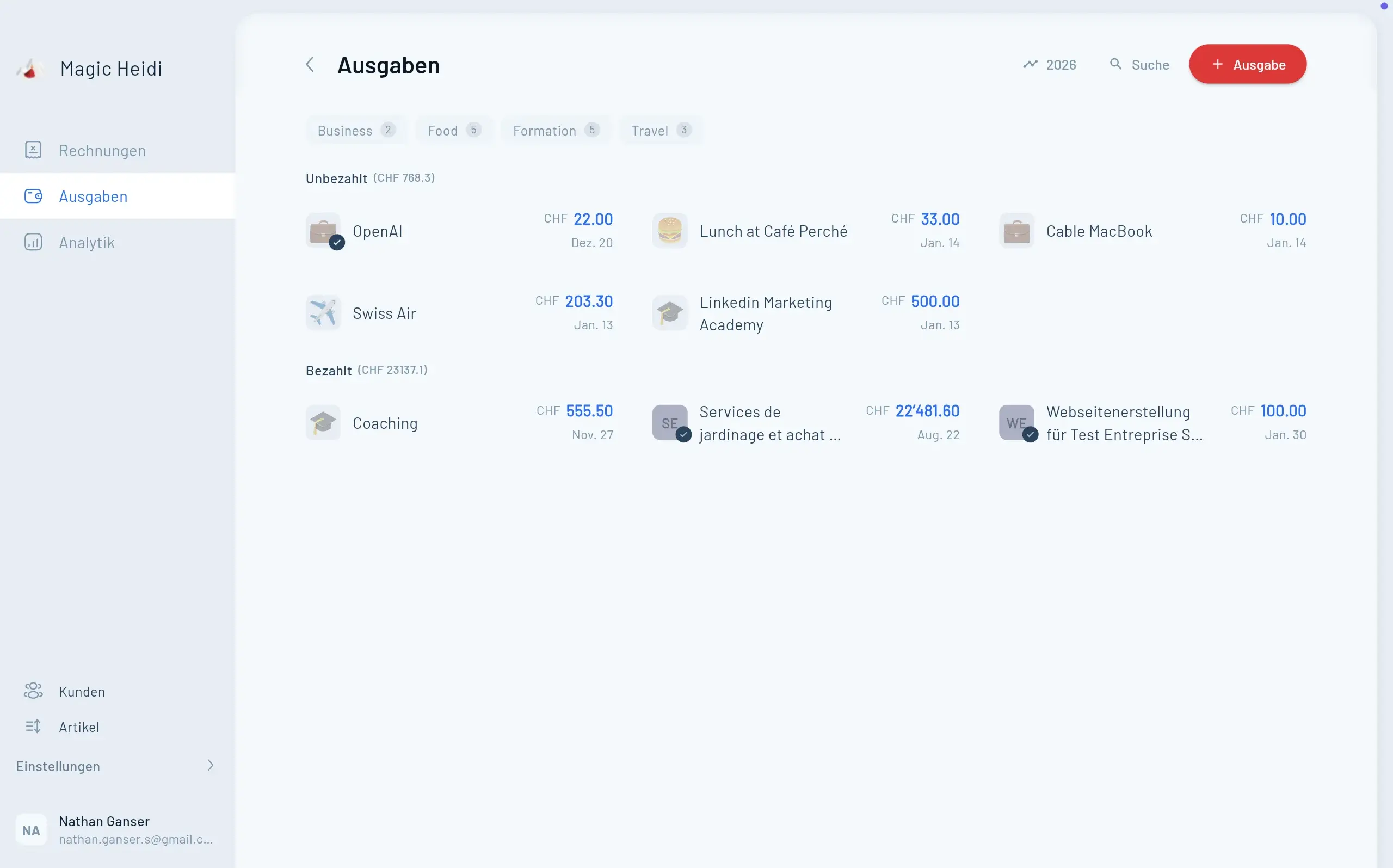

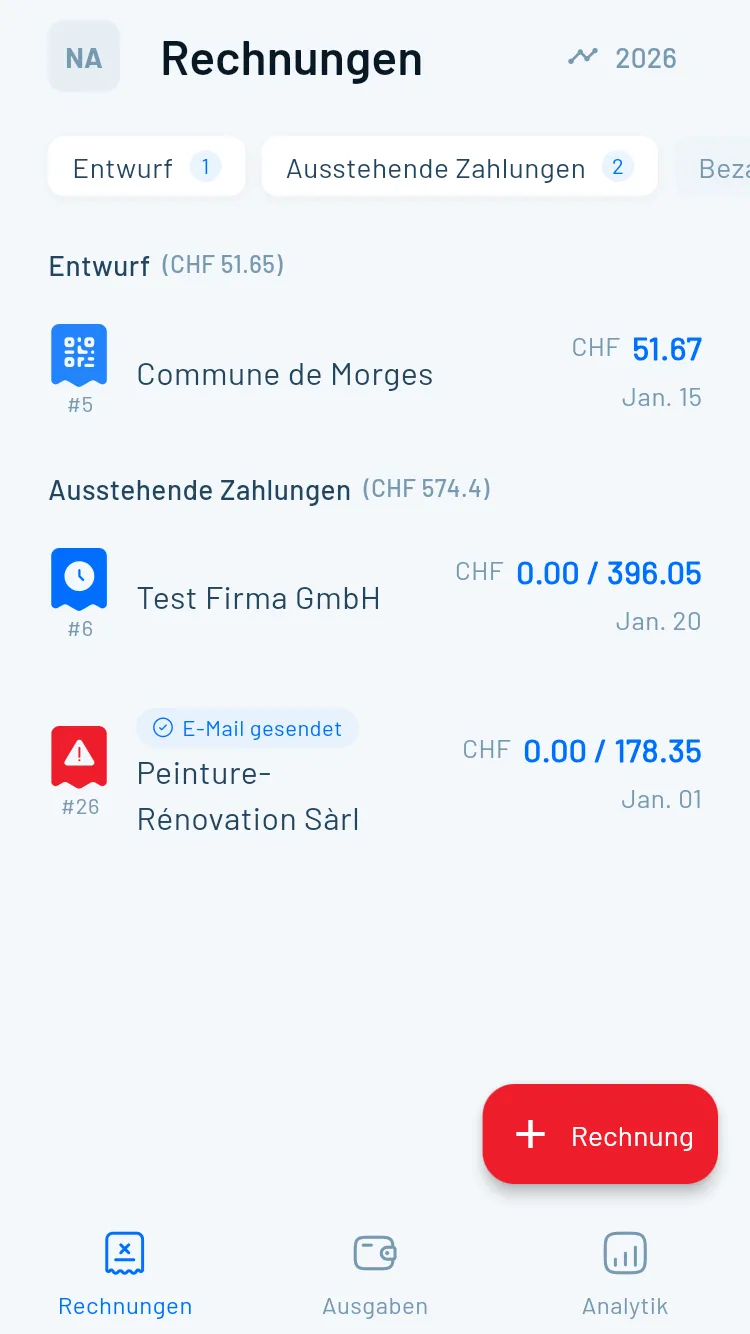

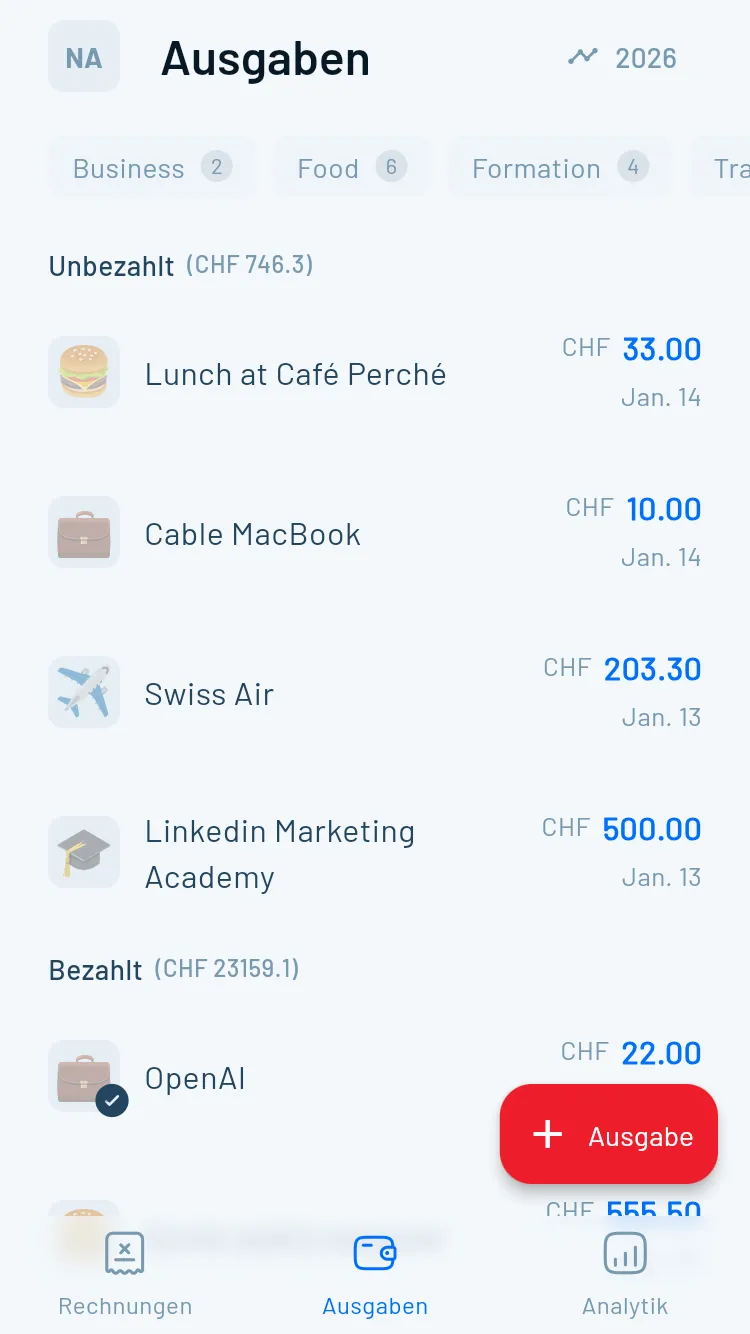

Sie benötigen vollständige Aufzeichnungen für das gesamte Geschäftsjahr

- Alle vier Quartals-MWST-Abrechnungen des Geschäftsjahres

- Vollständiger Jahresabschluss (Erfolgsrechnung, Bilanz)

- Alle ausgestellten Rechnungen (mit MWST-Beträgen)

- Alle Spesenbelege (mit abzugsfähiger Vorsteuer)

- Kontoauszüge mit tatsächlich erhaltenen und geleisteten Zahlungen